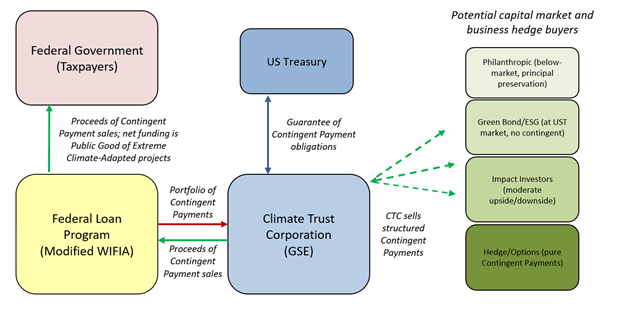

As noted at the end of a prior post on innovative infrastructure-related innovation, a straightforward way to inspire more innovation in the uses of WIFIA loan benefits is simply to combine data sets.

The key elements are data about current and selected WIFIA projects (plenty of that online from EPA and local water systems), data that might be relevant to the affected communities (ranging from economic statistics to climate exposure – also widely available) and estimates of the financial value of WIFIA loan benefits connected to the project’s financing.

This last data set defines the funding that might be available for innovative initiatives, so it’s obviously the core element of inspiration for any realistic plan. But estimates for the actual value of WIFIA loan benefits are not directly available. Press releases for WIFIA financings often include simple totals of interest rate savings, but this is not the same as the type of value required to establish additional funding capacity, which is the real point. In any case, press releases are (understandably) not going to follow a rigorous or consistent methodology in the numbers they report.

Fortunately, however, since the relevant WIFIA borrowers are all highly rated public water systems, there’s plenty of raw material from publicly available financial information to model WIFIA loan value estimates accurately, if not precisely. A standardized model, with specific project and borrower data input for the variables, will provide a uniform and consistent approach. It’s also a practical and efficient way to generate value numbers for the dozens of individual projects involved. This part of the exercise, though it involves an extra step, is pretty straightforward too.

Piles of statistics and financial numbers are…well, not exactly the best material to spark fires of innovation, however important they might be for actual implementation and consensus-building. But since a WIFIA financing is ultimately grounded in a physical project, with a specific real-world location and a clearly defined zone of impact, the piles of data can be anchored around a physical place. The obvious way to start with data visualization in this case (the kind of presentation that does spark innovation) is a map overlay. The graphic at the top of this post shows what some elements might look like – the base layer is the WIFIA project itself and the top layer is the WIFIA loan benefit value. The layers in between are where the inspiration and innovation happen.