Let’s face it: the standard Value for Money (VfM) evaluation for non-traditional infrastructure procurement and financing doesn’t work very well in the US.

VfM’s ongoing failure manifests itself in various ways but I think there’s fundamentally one ultimate cause. An infrastructure project intrinsically involves a complex bundle of benefits and costs, and P3-type alternatives are often sold as a bundle of contractual and financing components. All of the factors are very different, yet the VfM framework seeks to combine them into a projection of a single stream of cash and cash-equivalent values that is discounted by a single rate to produce a single “universal” number, the project’s PV of cost.

This explains what we see – and what everyone complains about: a VfM analysis is complex, expensive and not very useful. But is such a unitary approach to evaluation necessary?

Something like a unitary analysis may in fact be necessary when the infrastructure alternative being considered is a full privatization or demand-charge P3 that involves a significant transfer of ownership and control. In those cases, the deal is intrinsically bundled and the decision is basically whether “to sell or not sell”.

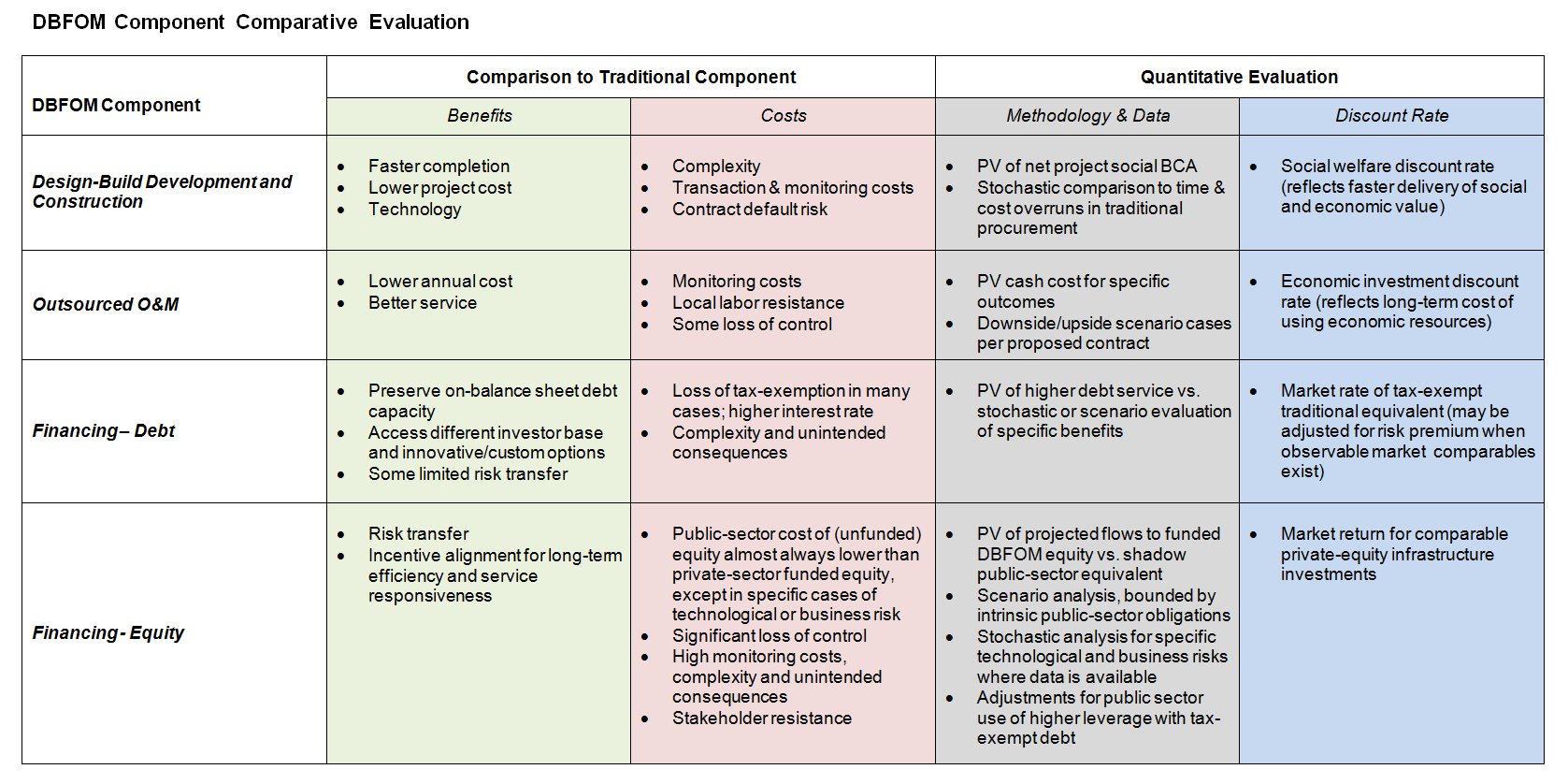

But non-traditional alternatives are often sought to improve only specific aspects of an infrastructure project, something that’s currently reflected in the alphabet-soup of P3 taxonomy: DB, DBF, DBFOM, etc. In these cases, a separate evaluation of each component of the proposed alternative with respect to its impact on a specific aspect of the project would appear to be a simpler and more practical approach. Non-traditional alternative evaluation would then involve multiple separate analyses, each using the appropriate “apples-to-apples” methodology with its own “natural” discount rate. I think this would not only lead to clearer and more useful results (both for decision-making and communication with stakeholders) but also to cheaper and quicker modelling (a series of small standalone Excel models is much easier to create than a single large integrated model).

For example, a DBFOM proposal could be evaluated with four separate models (click on to enlarge):

Something like this is clearly already being done when decision-makers choose to include or exclude components of a P3 (e.g. choose a DB deal only and exclude financing and O&M in the P3). Why not focus development efforts on improving and standardizing evaluation “modules” instead of further refinement of an already-too-complex VfM methodology?

The case for separate component evaluation becomes even clearer when the overall approach to non-traditional alternatives is explicitly based on providing a menu of options to the public sector, not on prepackaged P3 proposals. Each specific option would be proposed with its own custom-tailored evaluation methodology. Here’s what that might look like for the debt capitalization options described in the CMT approach (click on to enlarge):